The Financial Red Flags Quietly Costing Expats Thousands: How to Break Up With Your Financial Situationships

Let's talk about your dating history.

Not the human one (I won’t go there)... We don't have all day 😅.

I mean your financial dating history.

If you're anything like the expats I sit down with every week, your money has been through some absolute state of affairs. A string of relationships that looked promising and ended with you a little poorer and a lot more cynical than you wish to be.

Let me tell you, you're not a financial disaster, you just kept falling for the wrong types.

So pour the tea, let's go through your exes one by one. With love, and zero judgement (well okay, maybe just a little 😜).

First, what even is a financial situationship?

A situationship is that murky in-between. You're sort of together, but you never feel safe or secure. There's no commitment, no clarity, and a quiet little knot in your stomach that never fully goes away.

Your money has been living there for years.

You're earning a decent buck. Probably more than you ever did back home, but you don't feel free. You feel like you're winging it and hoping nobody notices.

That knot in your stomach? That's not a personality flaw, that's a relationship that was never built to make you feel secure.

Let's meet the culprits.

Ex Number 1: The Smooth Talker

You know the one.

The adviser in the designer suit who bought you an expensive coffee and promised you the moon and said all the right things. They made you feel like you'd finally met someone who understood your money.

Then he locked you into a 25-year "savings plan" with fees so high they're quietly funding his next car upgrade, not your retirement.

Big promises... Zero accountability… Gone the second the contract was signed.

The lesson hiding in the heartbreak: if something is sold to you hard, with a long lock-in and a charming face, your radar should go off. High fees are the silent killer of long-term wealth. They don't feel like much in any single month, but over decades they eat a frightening chunk of what should have been yours.

If you've ever felt that sick "wait, am I trapped in something?" feeling, you're not being dramatic, you're wide awake.

Whole Life Vs Term Life Insurance (The Showdown) for exactly how these high-commission plans drain you, and how to get out.

Ex Number 2: The Crypto Bro Bestie

"Bro, it's literally guaranteed."

You hadn't heard from them since the 50% drop, conveniently right after they told you to "get in" at the all-time high.

This one wasn't malicious, they really believed their own hype. That's almost worse, because the confidence was contagious and you caught it.

The lesson: there is no such thing as guaranteed, and FOMO is not a strategy. Betting your future on one hot tip from a pal, one coin, one "can't lose" sector is how people lose the whole lot. Real wealth gets built the long-term consistent way. Spread across thousands of companies, not stacked on one shiny promise.

Excitement and wealth-building rarely live in the same house. If an investment gives you a buzz, be suspicious. The good stuff is gloriously dull.

Ex Number 3: The Bank That Ghosted You

Ah, the slow fade.

Lured you in with a "great" introductory savings rate, made you feel chosen. Then quietly dropped it to 0.2% the moment you stopped paying attention.

You're still technically together, you just feel a bit invisible now.

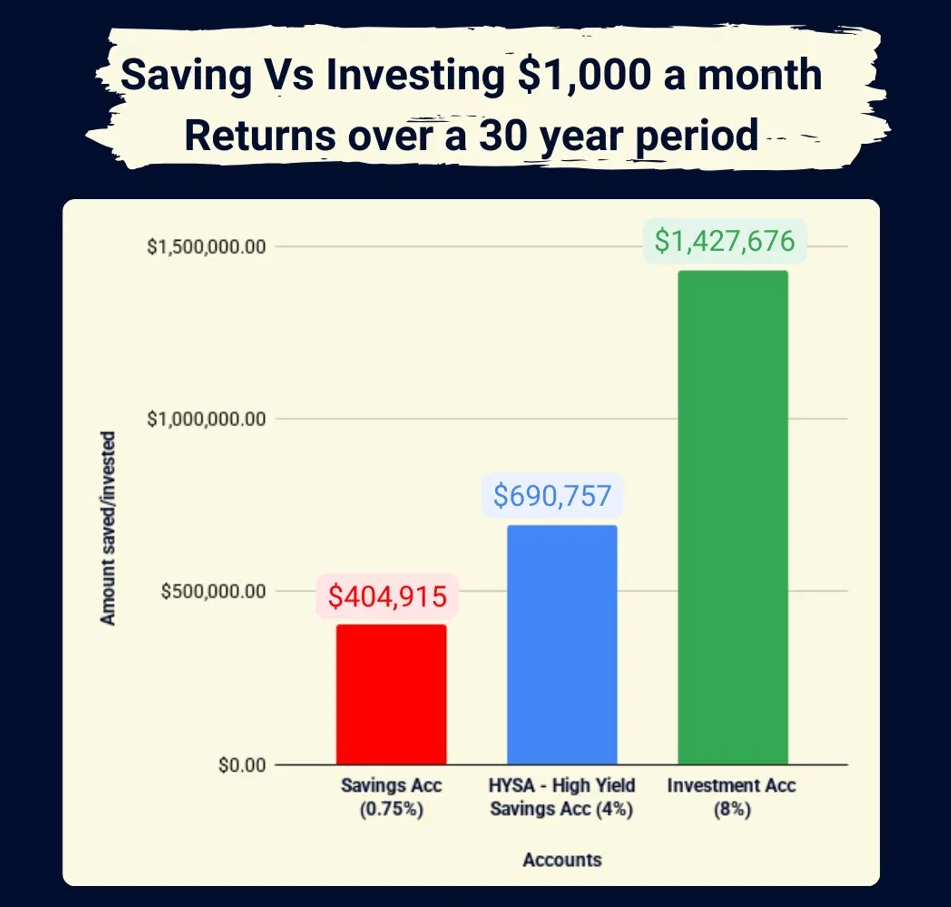

The lesson: cash in a low-interest account feels safe, but inflation is nibbling away at it every single year. Your balance looks the same on the screen while it quietly buys you less and less. Safe is not the same as smart.

Saving has a job, and it's an important one. It's your safety net, but it was never designed to build you a future.

Why Playing It Safe With Your Money Is The Riskiest Move Of All.

So why do we keep going back?

We certainly don't stay in bad money relationships because we're stupid. We stay because money was never just about numbers.

It's about safety, self-worth and control.

It’s the quiet fear of repeating whatever financial chaos, or financial silence, we grew up around.

For some of us, money was the thing the adults whispered about behind closed doors. For others, it was the thing nobody ever spoke of at all.

So we settle and we tell ourselves we'll sort it "another day". We stay in the situationship because at least it's familiar, and at least it doesn't ask anything of us.

I know, because I was that person too. "I'll invest when I have more time, when I earn more or when things settle down."

Spoiler: none of those arrived on schedule, they never do.

The day I stopped settling was the day everything changed.

What a healthy relationship with your money actually looks like

Here's the good news. You can absolutely build something steady, secure, and yes, a little bit sexy with your money.

A healthy money relationship has very different energy from the situationship.

Allow me paint it for you.

It's a bit boring, on purpose. No drama, no 2am panic, no checking the charts like you're checking if he's read your message. It’s just low-cost, globally diversified index funds, quietly doing their thing.

It shows up consistently. Just like a real partner doesn't disappear the moment things get a little volatile. You set up an automatic transfer shortly after payday and treat it like rent, your emotions don't get a vote.

It doesn't bail when things get hard. When the market has a bad day, and it will, you don't run, you stay. The ones who panic and leave at the first dip are the ones who get hurt. The ones who stay through the seasons are the ones who win.

Why the Stock Market's Wild Ride Is Your Best Ticket to Financial Freedom for why the dips are nothing to fear.

It's real, this isn't a casino. When you own a global index fund, you own real slices of real businesses, all over the world, all quietly working while you get on with your actual life.

This is the long-term, committed, ride-or-die relationship. The one that won't ghost you, won't cheat on you with crypto, and won't vanish the moment things get volatile.

How to make the first move

Ready to leave the situationships behind? Here's how you start.

1. Audit your current relationships. Dig out every plan, policy and account. Find out what you're actually paying in fees and whether you're locked in. You can't leave a relationship you won't look at honestly.

2. Build your safety net first. Ideally 3 to 6 months of essential expenses, somewhere safe and accessible like a High Yield Savings Account. This is the foundation everything else stands on.

3. Automate the good stuff. Set a monthly transfer into low-cost, globally diversified index funds. Make the decision once, then let it run. We're all busy, we all forget, remove the decision and you remove the self-sabotage.

4. Write your own vows. One short rule, written down before the next storm hits: "When markets drop, I will not sell. I'll keep investing and review my plan quarterly." Your calm self writes the rules so your panicked self can't break them.

That's it. Nothing flashy, or too complicated, it’s just steady, faithful, and built to last the distance.

The vision

Close your eyes for a second and meet future you.

Your calm, grounded, the rent or mortgage is paid from a place of strength, not stress. Your choices come from confidence, not FOMO or from external inflence. You can say no to the BS, walk away when you need to, and sleep soundly knowing your money is finally working for you instead of against you.

You got there because one ordinary day, you decided you were done settling for less than you deserve.

You stopped winging it, you committed, you showed up, again and again, even on the days it felt boring.

One day you'll look back and quietly say, "thank you for staying the course."

Because your money deserves a love story too.

If you're reading this thinking "right, it's time I finally got a proper plan," that's exactly what I'm here for.

It's 1:1 coaching built around you, your life, and your goals. No judgement, no designer suit and no man talking AT you. Just someone in your corner who actually listens, and an Irish accent you'll hopefully understand.

Let's chat: find me here and tell me where you'd love your finances to be in 6 months.

Not quite ready for that? Join the Wednesday Wisdom newsletter and I'll send you my free Beginner Blueprint. It's my own starter journey, step by simple step 😉

Educational purposes only. Not financial advice. Invest according to your own goals, timeline, and risk tolerance.

FAQs

1) Is it really that bad to leave my money in a savings account? Not bad, just not the full job. Savings keep you safe in the short term. They're not built to grow your wealth over decades, because inflation chips away at cash every year. Use it as your safety net, not your whole plan.

2) How do I know if I'm stuck in a high-fee plan? Look for long lock-in periods, hefty surrender penalties, and an "adviser" who earned a big commission for selling it to you. If you're unsure, dig out your policy schedule and surrender value and get a second opinion.

3) Do I need a lot of money to start investing properly? No. You need consistency, not a lump sum. Small, regular, automated amounts over a long time horizon do the heavy lifting. Time in the market matters far more than the size of your first deposit.